Leia este post em português

Two updates for today:

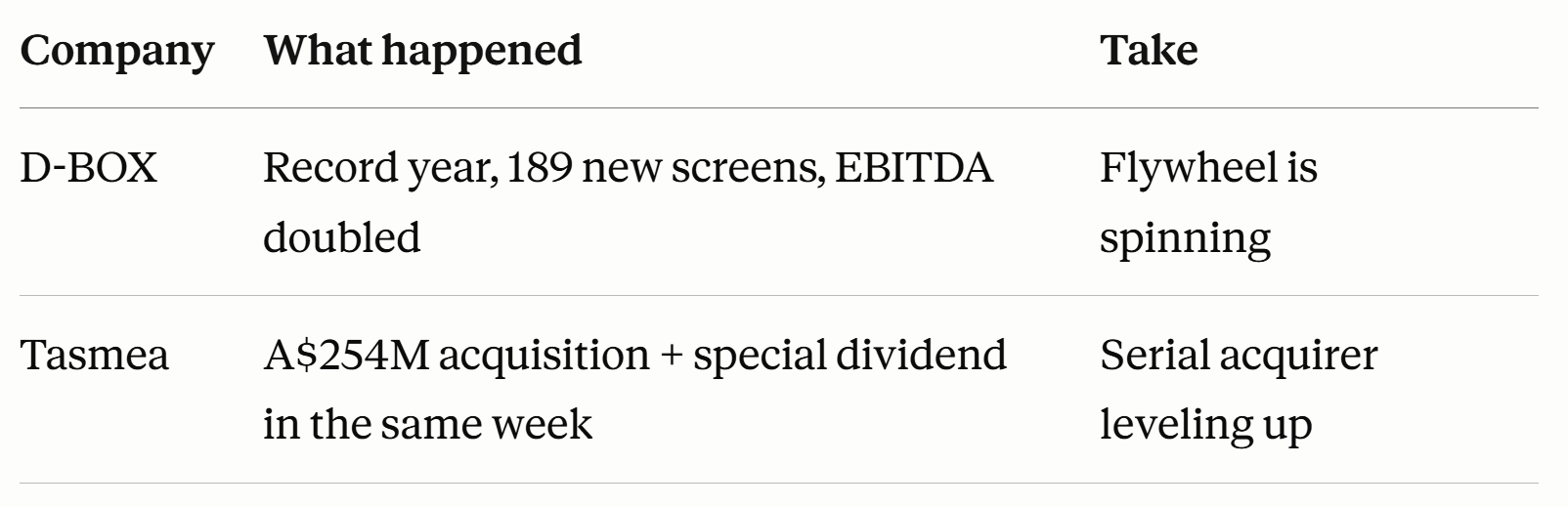

1) D-BOX Technologies (TSX: DBO)

D-BOX reported its FY2026 results. Let's take a look at what the company delivered and get to know the business a little better.

The numbers

FY2026 revenue: CA$57.6M (+35% YoY) - record year

Q4 revenue: CA$14.7M (+70% YoY) - strongest quarter in the company's history

Adj EBITDA FY2026: CA$15.5M (+112% YoY), with a 27% margin (up from 17% in FY2025).

Net new screens added: 189 (66 on Q4) - record

Cash: CA$17.6M, debt: near zero

NCIB in place

The flywheel

D-BOX designs, manufactures, and commercializes haptic motion systems for cinemas, sim racing, and training/simulation applications. Today, the company's primary focus is expanding its cinema footprint. Each new screen becomes a high-margin royalty asset, generating recurring revenue from every ticket sold with virtually no incremental cost. This year, total royalties grew 32% while the North American box office grew only 7%.

That gap kind of summarizes the thesis. The installed base is expanding so much faster than ticket sales can fluctuate that total royalties are outgrowing the box office by a wide margin. Growth is increasingly driven by screen count, not just by how many people went to see The Devil Wears Prada or whatever.

Exhibitors are treating D-BOX as a capital allocation priority to maximize yield per seat. In the CEO's words: "D-BOX is a highly deployable premium experience that can help maximize per-patron yield by delivering a uniquely immersive experience for audiences of all ages."

More screens → more royalties → more cash → more screens, with fixed costs diluted along the way. The model is self-reinforcing and the loop is working.

Changes in 2026

First, D-BOX announced in FY2026 its share repurchase program, up to ~9.5% of the float. The fact that management feels comfortable repurchasing stock while still adding screens at record pace says something about where they think the business is. The language in the release shifted to "disciplined capital allocation focused on creating long-term shareholder value".

Second, operating expenses grew 6% while revenue grew 35%. That's not cost-cutting. That's a business model revealing its true operating leverage. EBITDA margins went from 17% to 27% in one year.

What to watch

Not everything is clean. Sim racing and simulation both declined for a second straight year. Together they shrank from 44% to 28% of revenue. But that is somehow expected, as D-BOX is quietly undergoing a structural mix shift.

Q4 gross margins compressed 600bps because system sales (aka 'lower-margin hardware') dominated the mix, representing 53% of Q4 revenue versus ~12% a year earlier. Entirely justified by the strong pace of installations.

Looking into FY2027, I am following the pace of net screen additions, the growth of the royalty base relative to the box office, and the execution of the newly authorized buyback program, which has the potential to create meaningful shareholder value.

The bottom line

D-BOX underwent a complete management overhaul in 2025. Following a three-year activist campaign led by Daniel Marks, the board was replaced and a new CEO and CFO were appointed within months of each other. The strategic shift was decisive. Rather than prioritizing hardware sales, management refocused the entire business on its royalty engine.

The results have been hard to ignore. The key question is whether the record addition of 189 screens this year represents a new baseline or a peak. The opportunity suggests substantial runway ahead. North America alone has roughly 42,000 cinema screens. Globally, there are more than 200,000. D-BOX is installed in just 1,200 of them, which is less than 1% of the global market.

At ~13x ttmEBITDA, the market does not seem to be pricing a royalty engine compounding at 25%+. And there's also a tax shield, meaning D-BOX won't pay taxes for what I think is a little more than a couple years. Bad for the government, good for shareholders.

The most common concern is customer concentration. Cinemark appears to represent around half of all active screens and the bulk of recent additions. If that single relationship stumbles, the growth story stalls. I'm not very worried about that. D-BOX delivers strong ROIC for exhibitors, so theaters have real economic incentive to keep and expand the partnership. And the company is actively diversifying. On June 3rd, D-BOX announced a new partnership with B&B Theatres. Still, landing a second major chain like AMC would transform this from a concentrated relationship into a genuine platform. Until then, it's worth acknowledging the risk.

All in all, FY2026 was a strong year for D-BOX and further evidence that the transformation is working.

2) Tasmea $TEA.AX

Tasmea is an Australian specialist industrial services company that owns and operates multiples services businesses across mining, energy, infrastructure, water, and defense. Think of it as a serial acquirer of essential maintenance and electrical contractors. A seriel acquirer of small, owner-led businesses bought at modest multiples and run under a decentralised model. Tasmea is a nice company led by its competent co-founder, Stephen Young.

Well, this nice company made two announcements in the same week, and together they tell a clear story about where it is heading.

On June 2nd, the company announced the acquisition of Maxim Group, a specialist electrical contractor, for up to A$254 million (~5.4x EBIT). Maxim brings direct exposure to three of the fastest-growing infrastructure markets in Australia: data centres, battery energy storage and major government infrastructure. The business has grown revenue at ~70% CAGR over the past two years and carries a A$1.3 billion identified pipeline. Post-deal, Tasmea’s Electrical segment alone is expected to generate approximately A$100 million in EBIT. Forecast EPS accretion of 31% and net leverage stays below 1.0x. Very good deal, if you ask me.

Two days later, Tasmea declared a fully franked special dividend of 10 cents per share, with its Dividend Reinvestment Plan (DRP) available at AU$6.85 per share. At the same time, Tasmea reaffirmed its guidance and emphasized that the special dividend would not compromise growth initiatives or acquisition capacity. The sequence is telling. Just days after announcing the A$254 million acquisition of Maxim Group, Tasmea returned capital to shareholders while maintaining its growth outlook.

I thought the Maxim acquisition was excellent, and the market appeared to agree, sending the shares up more than 15% on the announcement. The stock has already nearly doubled this year and is now trading around all-time highs. Even so, the valuation may not prove demanding if Tasmea can continue acquiring high-quality earnings at attractive multiples as it did with Maxim.