• Facebook")

CLIQUE AQUI PARA LER EM PORTUGUÊS

Website: https://www.ziffdavis.com/

Ticker: ZD 0.00%↑

Ziff Davis is a digital media and internet services company that operates a portfolio of online brands focused on technology, shopping, cybersecurity, entertainment, health, and digital marketing.

The Ziff Davis of today traces its roots to J2 Global, an email-to-fax business founded in 1995. After surviving the dot-com bust, J2 turned its strong cash generation into an acquisition machine. The Ziff Davis brand itself was one of those acquisitions.

In 2010, digital media executive Vivek Shah and Great Hill Partners acquired the company, which had recently emerged from bankruptcy. Just two years later, they sold it to J2 Global for a nice profit.

Shah remained in charge of the digital media division before becoming CEO in 2018. In 2021, the company spun off its legacy fax business into Consensus Cloud Solutions and began operating under the Ziff Davis name, adopting the brand it had acquired years earlier.

A SALE THAT CAUGHT OUR ATTENTION

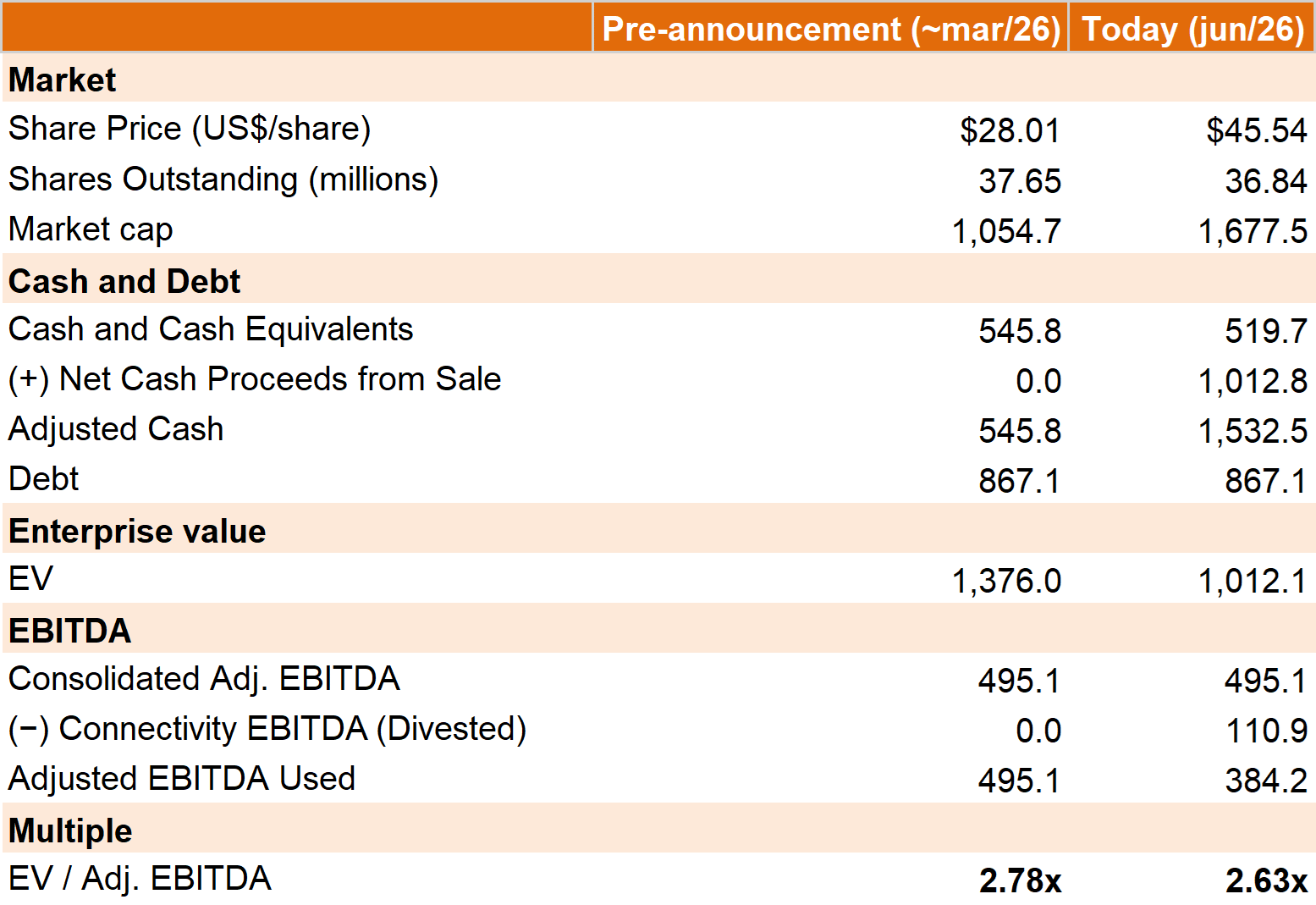

In March, Ziff Davis announced the sale of its Connectivity business for $1.2 billion in cash. The transaction closed last week and stood out for a simple reason: the asset was sold for roughly 11x EBITDA, while the entire company was trading at around 3x EBITDA.

In other words, a single segment was sold for a value close to the enterprise value of the entire company. For the first time, investors were able to see what a strategic buyer was willing to pay for one of the businesses inside the portfolio.

The stock reacted, to be fair. It jumped nearly 50% on the day of the announcement and has moved somewhat higher since. But a closer look suggests the reaction was surprisingly muted. The market acknowledged the sale, yet continues to assign little value to the rest of the company.

Vivek Shah appears to share the same view. On the company's May call, he summed up his frustration as follows:

“So we announced the sale of the connectivity business for $1.2 billion, stock responded, but only responded literally equal to the cash proceeds of the transaction, meaning that the remaining close to $400 million of EBITDA might have actually compressed

Might have compressed the multiple, which is disappointing because it's -- that shouldn't be the conclusion that anyone draws. And so we're going to continue to focus on the opportunities that presents, and that includes buybacks, and we've been very consistent about that, but also asset monetization”, Vivek Shah

BUYBACKS & ASSET MONETIZATION

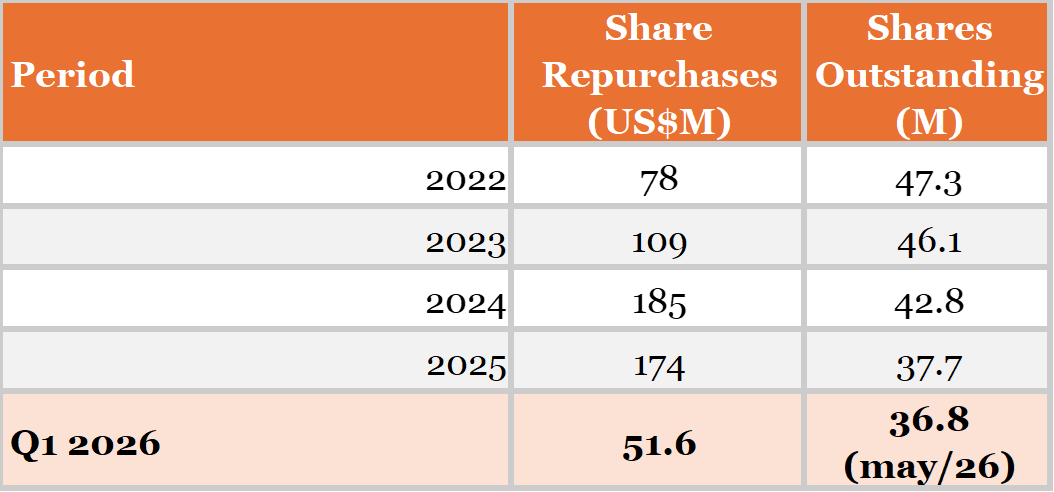

Vivek Shah is not overstating the case when he points to Ziff Davis's track record of buybacks. Over the past several years, the company has repurchased nearly a quarter of its shares outstanding.

With healthy annual free cash flow of roughly $300 million, Ziff Davis has never lacked the firepower to support its ongoing buyback program. Without Connectivity, that cash generation will inevitably decline. On the other hand, more than $1 billion in net proceeds has just been added to the balance sheet.

Before considering what management might do with that cash, it is worth revisiting the second part of Vivek Shah’s comment: asset monetization. To understand what he meant, it helps to take a closer look at Ziff Davis itself.

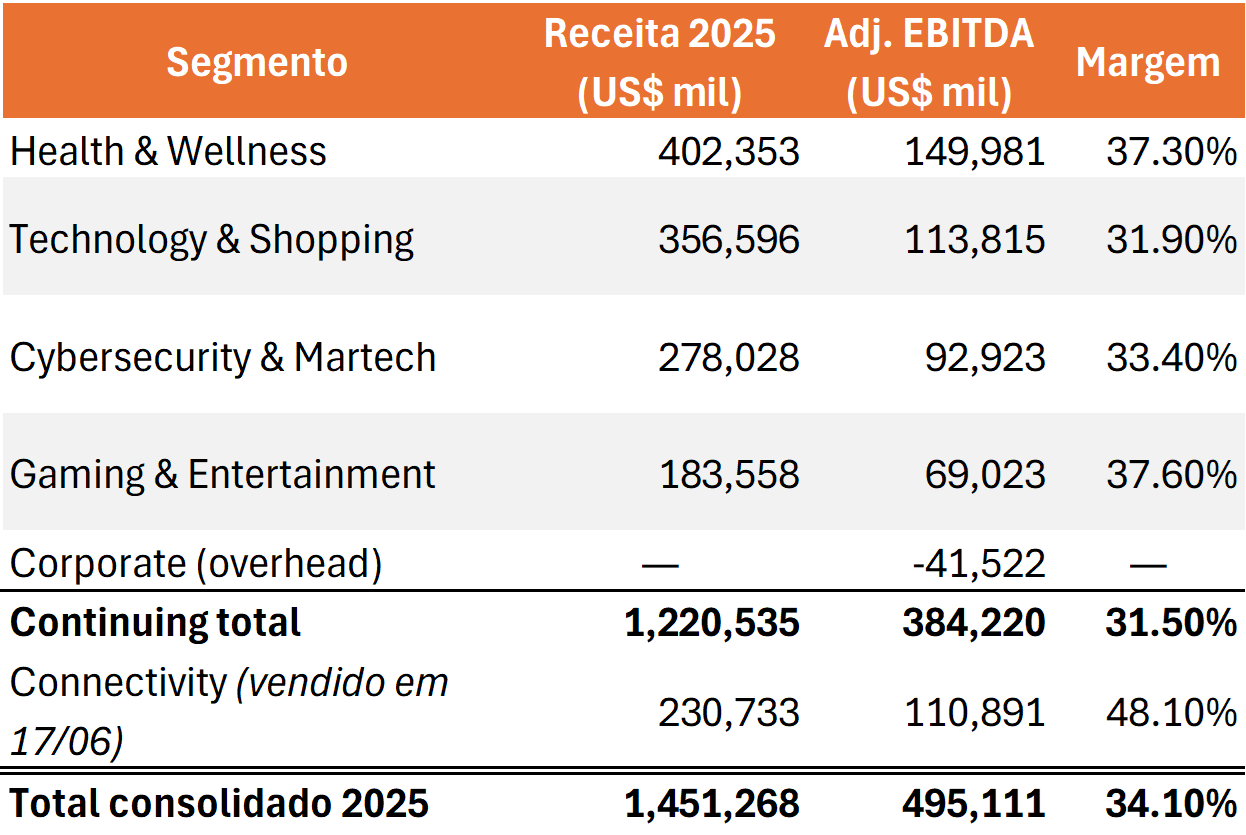

Connectivity was also the company's highest-margin segment (48%), which helps explain why it was sold for roughly 11x EBITDA.

Health & Wellness is now the company's largest segment by both revenue and EBITDA, as well as its fastest-growing business (+11% in 2025). The segment operates across three verticals: consumer health (tools and apps such as Lose It!), professional and medical media (MedPage Today), and pregnancy and parenting (BabyCenter and What to Expect). Growth is driven by pharmaceutical advertising, data, and partnerships with leading medical institutions such as the Cleveland Clinic.

Technology & Shopping is the segment most exposed to AI disruption, with revenue declining 13% in Q1 2026. The portfolio includes well-known brands such as CNET, PCMag, Mashable, and RetailMeNot. Revenue is generated through advertising, affiliate commissions, and sponsored content.

Gaming is the highest-margin segment among the remaining businesses, with a margin of 37.6%, and continues to grow. Its portfolio includes brands such as IGN Entertainment, one of the world's largest gaming websites, and Humble Bundle, a digital storefront and subscription service for video games.

Cybersecurity & Martech is a stable, subscription-based business with recurring revenue.

Anyone looking at Ziff Davis's stock price could be forgiven for thinking the company is in terminal decline. The reality, however, is quite different. Revenue remains stable, the business is profitable, generates substantial cash flow, and owns a portfolio of valuable digital assets.

Beneath the surface, however, it becomes clear that not all of those assets are created equal. Some face genuine challenges, while others continue to perform well. Vivek's frustration is that the market seems unwilling to distinguish between them, valuing the strongest businesses as though they were no different from the weakest.

Selling assets at fair valuations becomes a way to unlock that disconnect. It is a capital allocation approach that I find particularly appealing. That is exactly what happened with Connectivity, and all indications suggest that Vivek is willing to continue following the same playbook.

"We recognize that we own some businesses facing headwinds and that require turnarounds. However, we believe that we also have businesses worth well in excess of what our current stock price implies. The market appears to be penalizing the better-performing businesses in our portfolio for sharing an ownership structure with those that are under pressure." Vivek Shah

If I were Vivek, I would keep a close eye on Health & Wellness. It is a high-quality asset operating in a sector where both strategic buyers and private equity firms remain active. It is not hard to imagine the business commanding a valuation of around $1.5 billion in a sale—an amount that would be close to Ziff Davis's entire current market capitalization.

CAPITAL ALLOCATION

And what could management do with all that cash?

"...we will evaluate the best use of proceeds for the benefit of our shareholders. Possible options include reevaluating the leverage on our balance sheet, repurchasing shares, exploring dividends and reinvesting in our businesses through M&A or other general corporate purposes.", Vivek Shah

1. Debt reduction. Ziff Davis currently carries roughly $870 million of debt, of which about $150 million is short-term. The debt was neither burdensome nor difficult to manage even before the Connectivity sale. Now, with more than $1 billion in cash proceeds, it becomes far less significant. Given this recent asset monetization, I would expect management to pursue at least some degree of deleveraging.

2. Share repurchases. This is a capital allocation lever management has been pulling for some time now. On the first-quarter earnings call, the company made it clear that it intends to remain an active buyer of its own shares. With fresh cash added to the balance sheet and a strong belief that Ziff Davis trades well below its intrinsic value, I would expect the pace of buybacks to accelerate.

3. M&A. Acquisitions are deeply embedded in the company's DNA. The playbook has always been the same: acquire assets, improve them, generate cash flow, and earn attractive cash-on-cash returns. Even so, the most recent deals—Popular Science, Dwell, Domino, and Business of Home—have been relatively small. According to management, each was completed "for an adjusted EBITDA multiple that is accretive to our own."

That said, I would be hesitant to see Ziff Davis pursue an acquisition-heavy capital allocation strategy. Fortunately, there is little evidence that management is moving in that direction. In recent years, the company has consistently allocated more capital to share repurchases than to acquisitions.

4.Dividends. Vivek has mentioned dividends as a possible alternative, although only in passing. As far as I can tell, they have never been part of the company's historical capital allocation playbook. Even so, a distribution would be welcome. That is particularly true given the size of the proceeds from the Connectivity sale and the potential for additional cash inflows should the company continue monetizing assets from its portfolio.

WRAPPING UP

At the end of the day, this is a capital allocation story.

The value of Ziff Davis’s assets is real, and the sale of Connectivity at roughly 11x EBITDA provides tangible evidence of that. The question that will ultimately determine investor returns is not whether the business is worth more than its current valuation. It is whether management can successfully translate that underlying value into shareholder value.

That is Vivek’s job from here: to narrow the gap between what the business is worth and what the market is willing to pay for it. And, ultimately, to ensure that value finds its way back to the people who own the company.

And that is precisely what he has been signaling. Asset monetization is now part of the ‘toolkit’. He has reaffirmed that the company remains an ‘active repurchaser’ of its own shares and has been explicit in stating that he believes the stock trades below its intrinsic value.

Vivek even invokes Ben Graham to describe the game from both sides:

“The intelligent investor is a realist who sells to optimists and buys from pessimists.” — Vivek Shah, citando Ben Graham

Why does the market punish Ziff Davis so severely? It’s a fair question. At first glance, I can think of three reasons.

The first is the narrative anchor that AI is killing digital media. Even though only a portion of the business is under pressure, that narrative tends to spill over to the entire portfolio.

The second is a complexity discount. The company spans five different segments, and its financial statements are cluttered with impairments and discontinued operations. For many investors, it's simply easier to move on to the next ticker.

The third is a classic "show me first" mentality. The market seems to want more tangible evidence of how this value will be unlocked and ultimately returned to shareholders. For investors unwilling to underwrite management’s intentions, a formal strategic review with clear objectives and timelines could go a long way toward reducing that skepticism.

I believe that if management executes this capital allocation playbook successfully, Ziff Davis could undergo a meaningful re-rating. In many ways, the situation reminds me of PBI, a company I have written about extensively. The parallels even extend to the short interest. To this day, roughly 15% of Ziff Davis’s float remains sold short.

The difference is that my confidence in Kurt Wolf was materially higher than my confidence in Vivek. That is not meant as a criticism of Vivek. It says more about my assessment of Wolf as a capital allocator than it does about any perceived shortcomings on Vivek’s part.

Even so, the current discount and the asymmetry of the opportunity may be enough to compensate for that gap in confidence.

Who knows?

See you outside the index,

Leo Caroli